FTR update: Mixed trends for freight rail

6/20/2023

By Julie Sneider, Senior Associate Editor

So far in 2023, rail carload volume growth has been slow and steady, but intermodal volumes still have a way to go before they get back to historical norms.

That was the prognosis from Todd Tranausky, vice president of rail and intermodal at FTR Transportation Intelligence, who spoke about carload, intermodal and port trends during FTR’s June 8 webinar, “2023 Key Issues in Transportation.” The other event speakers were FTR Chairman Eric Starks and FTR VP of Trucking Avery Vise.

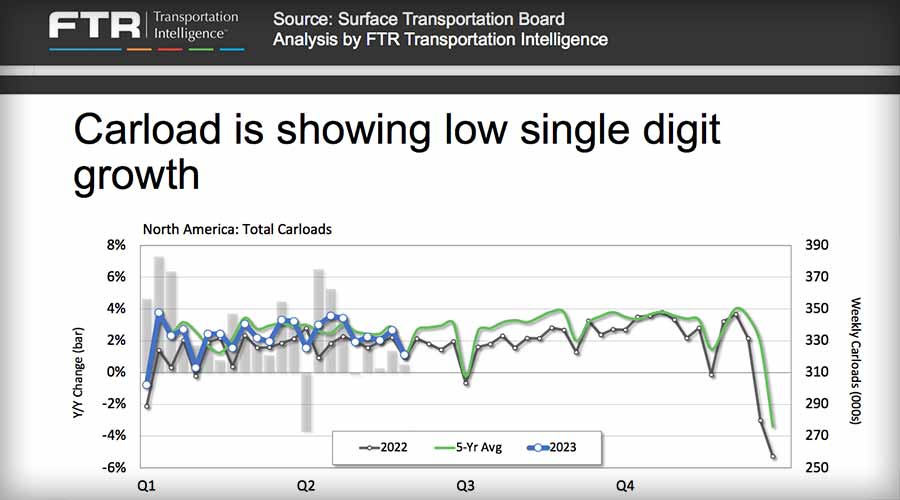

According to Tranausky, the state of the freight-rail market is mixed. For example, carload volumes so far this year are performing better than expected, with increases generally in the low single digits compared with what they were a year ago.

“They’re right in line with the five-year average, and we [at FTR] think that will remain through the balance of the year,” said Tranausky. Part of that is due to economically sensitive freight — commodities that are not coal, agriculture or petroleum products are doing better than overall carload categories, he said.

So far this year, carload volumes are better than expected, according to Todd Tranausky, vice president of rail and intermodal at FTR Transportation Intelligence. FTR Transportation Intelligence

So far this year, carload volumes are better than expected, according to Todd Tranausky, vice president of rail and intermodal at FTR Transportation Intelligence. FTR Transportation Intelligence“They are up 3, 4 or 5% on a year-over-year basis,” he said. “And that is a good sign. These are the commodities that will drive volume growth today, tomorrow, next year and for the rest of the decade.”

In his view, the economically sensitive carload commodities to watch include crushed stone, sand and gravel, and chemicals. The former has been a growth driver for the past 18 months, exceeding the five-year average as well as last year’s numbers by between 8% and 10%, he said. That growth is likely to continue “for some time to come” thanks to federal and state spending on infrastructure projects, Tranausky said.

Meanwhile, chemicals volumes have been a carload growth driver for the past five years and this year’s numbers are tracking last year’s trajectory. However, the category’s volumes have been down a tad over the past few quarters — a trend to watch closely.

“Chemicals go into so many industrial manufacturing processes, so if this [category] goes down, that would give us concern about what that might mean for the overall economy,” he said.

FTR’s intermodal competitive index, created with AAR data, shows that intermodal will continue to struggle with truck competition through 2024. FTR Transportation Intelligence

FTR’s intermodal competitive index, created with AAR data, shows that intermodal will continue to struggle with truck competition through 2024. FTR Transportation IntelligenceBut in terms of bulk freight, railroads’ largest carload commodity by volume — coal — has remained steady.

“If you look at it over the past six weeks, it’s been very flat, around 72,000 carloads,” Tranausky said. “This sort of defies economic logic, if you look at natural gas prices. There really isn’t a fundamental explanation for it. You would expect it to be doing a lot worse than it is.”

It’s unclear how the other key bulk commodity — grain — will perform volume-wise this year because of an early start to Canada’s wildfire season.

“There’s a lot of uncertainty about where grain will end up this year,” said Tranausky. “Many on the U.S. East Coast are aware of the fires in Canada, mostly in Quebec. The question is: As the summer goes on, do the wildfires spread out into the grain growing season? We’ll have to see how that evolves this year.”

Intermodal volumes continue to lag

As for intermodal, volumes remain weak despite a recent uptick in traffic. U.S. intermodal traffic was down 10.9% to 5,124,695 containers and trailers for the first five months of 2023 compared with the same period in 2022, according to Association of American Railroads data.

“Even though [intermodal] made some gains, we’re still down 10% compared to last year, where we’ve been for much of the year,” Tranausky said. “There’s a lot of work that remains in terms of intermodal getting volume back to historical norms. Unfortunately for intermodal, it doesn’t control all the factors that are pressuring its volumes.”

Among those factors are port shifts — more imports are arriving at Gulf, South and East coast ports and less at West Coast ports — and competition from trucking, he said.

U.S. port volumes — especially on the West Coast — have been trending down for months and are a major reason rail intermodal volumes have been on the decline in 2023, according to AAR data. Concurrently, FTR’s intermodal competitive index, created with AAR data, shows that intermodal will continue to struggle with truck competition through 2024.

“There’s a lot of work that remains in terms of intermodal getting volume back to historical norms.” — Todd Tranausky FTR Transportation Intelligence

“There’s a lot of work that remains in terms of intermodal getting volume back to historical norms.” — Todd Tranausky FTR Transportation IntelligenceTranausky also talked about shifts in market share of the various intermodal corridors. For example, market share of the Midwest-Southwest corridor, where freight moves out from Southern California toward and into Chicago, shrank from 20% in 2019 before the pandemic to 19.2% in 2022. The volume has now spread into other lanes.

“That corridor lost almost a full percent of intermodal market share. One percent may not sound like a lot, but it is a large amount of volume,” he said.

Also losing market share is the Southern California-to-Dallas corridor, as more volume shifts to Houston and Mexico. The big wild card will be the impact of the newly merged Canadian Pacific Kansas City and its ability to draw traffic over the U.S.-Mexico border, he added.

Ongoing labor issues and supply-chain factors that plagued the West Coast ports — prompting shippers to use ports in the East, Southeast and in the Gulf — also contributed to the shift. [Although a tentative six-year contract agreement between the International Longshore and Warehouse Union (ILWU) and the Pacific Maritime Association was announced June 15 after the FTR webinar], Tranausky noted it will take a while before the labor situation settles to see if intermodal volumes that moved East, Southeast and to the Gulf begin to return to the West Coast.

During the Q&A portion of the presentation, Tranausky was asked about import trends from countries in Southeast Asia outside of China.

“It’s one of the fastest-growing import areas,” he said. “Places like Vietnam and the Philippines are really growing at the expense of China, and that affects how freight moves. It makes more sense for those imports to come in via the Suez Canal to East Coast ports; whereas in China, the most efficient way to move freight out of the country is to Southern California.”

Also, as manufacturers continue to move their production from China to other locations, there’s an incentive to shift where freight comes into the country, which is away from the West Coast ports and into the East or Gulf coasts. Businesses that transitioned away from the West Coast may have found they like the change.

“Those folks may be thinking, ‘Hey, I kind of like the East Coast or the Gulf Coast because my length of haul is shorter, and now I can play with rail versus truck,’” Tranausky said.