2025 MOW Spending Report: Passenger-rail programs

2025 MOW Spending Report: Passenger-rail programs

Gardner steps down as Amtrak CEO

Gardner steps down as Amtrak CEO

Guest comment: Oliver Wyman’s David Hunt

Guest comment: Oliver Wyman’s David Hunt

Women of Influence in Rail eBook

Women of Influence in Rail eBook

Stay updated on news, articles and information for the rail industry

May 2021

Rail News: Kansas City Southern

Canadian Pacific-Kansas City Southern: Industry constituents weigh in on the proposed merger

By Jeff Stagl, Managing Editor

[Editor's note: KCS on May 21 announced it terminated the CP merger agreement and entered into a merger agreement with CN. KCS paid CP a breakup fee of $700 million, which will be reimbursed by CN. CP announced it intends to proceed to prepare and file its application with the STB seeking authority to control KCS and its subsidiaries.]

Tony Hatch was watching an NCCA men’s basketball tournament game late on March 20 and discovered an online Financial Times news story. Justin Long was alerted to breaking news the morning of March 21 after attending a wedding the night before. Allison Landry awoke that same morning to find more than 50 text messages on her smartphone.

That’s how three rail industry analysts learned Canadian Pacific and Kansas City Southern had forged a merger agreement. They were caught off guard — more so since the deal was announced over a weekend — but not stunned because KCS has been a merger target for about 20 years.

CP proposes to acquire KCS stock in a cash transaction worth $29 billion. The new entity Canadian Pacific Kansas City — which would be the smallest of the six Class Is — would employ nearly 20,000 people and generate $8.7 billion in annual revenue. The railroad would be headquartered in Calgary, Alberta and manage a 20,000-mile network in Canada, Mexico and the United States.

CP-KCS is the first agreed-upon Class I merger pact since 1999, when Burlington Northern Santa Fe Corp. and CN sought to combine and form North American Railways Inc. That attempt was called off in 2001 after the Surface Transportation Board (STB) implemented more stringent merger rules. Between 2014 and 2016, CP also launched unsuccessful attempts to force mergers with Norfolk Southern Railway and CSX.

CP President and Chief Executive Officer Keith Creel long has considered consolidating with another Class I and has garnered merger-attempt experience working under then-CP leader E. Hunter Harrison, says Landry, a senior equity transportation research analyst at Credit Suisse.

“In hindsight, [CP-KCS] really wasn’t too surprising. There are a couple of ways to look at it in a big picture,” she says. “They have no overlap — there isn’t even a single shipper that would go from three to two Class Is, or from two to one — and strategically it makes a lot of sense with a single haul to more markets.”

However, what has been somewhat surprising to rail industry insiders and observers is the myriad developments that followed the CP-KCS announcement, the biggest of which was CN’s unveiling of a rival merger proposal on April 20 (see sidebar near bottom).

Over the past month-plus, CP and KCS gained an STB decision to evaluate the proposed combo under pre-2001 merger regulations, honoring a KCS exemption that several Class Is and many shippers opposed; filed an objection with the STB stating CN-KCS doesn’t qualify for a major transaction waiver; garnered support from nearly 500 shippers and stakeholders; stated more than 110 customers and other parties object to or are concerned about CN-KCS; and advanced a necessary voting trust to be led by former KCS leader David Starling. In addition, KCS installed Executive Vice President of Operations Jeffrey Songer as EVP of strategic merger planning to manage the merger application process.

[Editor’s note: Since this cover story was published, the STB determined the voting trust agreement for CP-KCS is warranted and support for the merger reached about 550 shippers and stakeholders. In addition, KCS' board on May 13 determined CN's then-revised bid was a "company superior proposal" and opted to terminate the CP merger agreement.]

Meanwhile, CN in a shorter timeframe submitted a pre-filing to the STB; obtained assurances from KCS’ board they would engage in merger discussions; sent a letter to KCS constituents stating the merits of CN-KCS; elicited support from more than 700 shippers and stakeholders; and pursued plans to similarly install Starling as trustee of a CN-KCS voting trust.

[Editor’s note: Since this cover story was published, CN expressed support for the STB’s voting trust determination on CP-KCS since the board applied the same public interest factors CN believes should apply to both voting trusts, and announced more than 1,000 stakeholders now support CN-KCS, its voting trust or both.]

In the midst of all that, Creel and CN leader JJ Ruest have had heated exchanges on each other’s merger proposal, which at times included strong remarks about why one is superior or the other is fraught with peril.

What’s become a dizzying series of letters, filings, comments and retorts has challenged industry insiders and observers to keep up with the latest developments and weigh the ramifications. Following are some observations, concerns, predictions and best guesses surrounding that potential merger, with a smattering of comments on CN-KCS.

Just a jab

CP-KCS is about stabilizing the industry and combining the two smallest Class Is, which keep a “chip on shoulder” about their size, says Hatch, an independent rail industry analyst and Progressive Railroading columnist.

“They wouldn’t become so big they would hurt the others. It gives balance to the industry and keeps equal competition, with two large Class Is in the East and two in the West,” he says. “The merger is not a gut punch, it’s a jab.”

Until a calendar is released for the merger’s review, the combo is difficult to gauge, says Hatch.

“I want to see dates and how things will be done by STB,” he says. “And don’t just tell us about the [merger’s] potential synergies, I want the chance to analyze the growth and service opportunities. We only have a tone of that now.”

CP has released a short timeline showing it expects to file a preliminary proxy/registration statement with the U.S. Securities and Exchange Commission by early May, obtain a decision about closing into a voting trust and submit consideration documents to KCS shareholders by mid-2021, and learn the STB’s common control decision sometime in mid-2022.

CP-KCS would connect ports on all U.S. coasts via a single-line, continent-wide network, Garrett Holland, a senior research analyst at Robert W. Baird & Co. Inc., wrote in a March 22 report. Limited overlap — with only a single point of connection in Kansas City, Missouri — and the current interpretation of the STB’s governing rules favor the merger, he believes.

“We think deal approval is more likely than not,” Holland wrote.

Long, a transportation industry analyst with Stephens Inc., concurs.

“I like to use a basketball analogy. This one isn’t a layup, but it’s a free throw, so it has about a 75% chance,” he says.

Other Class I mergers face a lower-percentage chance — more like a three-pointer or half-court shot, says Long.

All in the cards

STB approval of CP-KCS could hinge on what Creel is willing to do, says David Vernon, an analyst with AllianceBernstein LP.

“Will he throw the open access card to address competitive concerns?” Vernon posits.

CP is offering the highest valuation ever for a rail transaction, about twice what Warren Buffett and his Berkshire Hathaway Inc. paid for BNSF, Vernon says.

“Keith has strapped himself to this transaction,” says Vernon.

Since CP long has employed precision scheduled railroading (PSR) and KCS has entered the second phase of PSR implementation, the merger is an opportunity to expedite growth in a proforma network, says Long. The combo is about exploiting revenue synergies and not about cutting, he believes.

“The railroads are conveying that it’s a combo forged on growth, which is different than mergers proposed in the past,” says Long. “With CP-NS, it was all about cost synergies and implementing PSR at NS. It would have reduced headcount.”

He finds it intriguing that CP-KCS hasn’t elicited much opposition. A shipper survey conducted by Stephens shortly after the merger was announced showed 76% of the respondents either supported or were indifferent to it.

“The 24% that are opposed to it was a lower percentage than I expected,” Long says.

Soliciting support

Hundreds of customers have submitted supportive letters to the STB, including such shipper groups as the Canadian International Freight Forwarders Association, Mexican Association for the Automotive Industry, National Importers & Exporters Association of Mexico and Transload Distribution Association of North America. In terms of opposition, the American Chemistry Council, Corn Refiners Association, Fertilizer Institute, National Grain and Feed Association, National Industrial Transportation League and U.S. Wheat Associates had petitioned the STB to revoke KCS’ presumptive waiver.

A number of railroads and holding companies also favor CP-KCS, such as the Montreal Port Authority, Port of New Orleans/New Orleans Public Belt Railroad, Genesee & Wyoming Inc. and Watco. But some railroads have been highly skeptical, such as Union Pacific Railroad, which expects to remain active and engaged in the merger’s regulatory process to protect its interests, ensure competition is enhanced and prompt the STB to use a level playing field when reviewing mergers.

The North Dakota Grain Dealers Association (NDGDA) figures to monitor CP-KCS closely, too. The 110-year-old association represents the interests of 160 grain elevators and has about 300 affiliate members.

The association supports CP-KCS because the merger would expand market access for North Dakota grain shippers and help make CP more competitive with BNSF, since they are the only two Class Is operating in the state, says NDGDA EVP Stu Letcher.

“We hear from members that it would open Mexico as a market for our wheat shippers,” he says. “It also could create grain moves to the Gulf Coast, which we don’t have now in North Dakota — a straight shot to the Gulf.”

Proceed with caution

However, the association is taking it at face value that the merger will open more markets for the state’s grain.

“If we ever hear it would cause a deterioration of service, we will oppose it in a hurry,” says Lechter.

Conversely, the NDGDA opposes CN-KCS because association leaders believe the merger would decrease rail competition and effectively end any opportunity to expand markets for North Dakota grain shippers who use CP.

The Soy Transportation Coalition also backs CP-KCS. The coalition includes 13 state soybean boards that account for 85% of total U.S. soybean production.

CP-KCS could result in greater access to new markets in the southern United States and Mexico, says Mike Steenhoek, the coalition’s executive director.

“It would produce a network that’s very similar to CN’s current network,” he says. “Both would be north-south into the U.S. and branch off to the West Coast of Canada. It would not create a new category of service.”

However, the coalition is always concerned about anything that would impact soybean shippers, says Steenhoek.

“The bottom line is we will wait to see what happens. We have witnessed other consolidation in the rail industry, and there have been occasions where mergers resulted in rate increases and service declines,” he says. “Those are still top-of-mind to ag shippers.”

In terms of CN-KCS, any red flags and alarm bells that usually occur with a proposed merger are more pronounced in that case, Steenhoek believes. The combo would create a much larger railroad and wouldn’t guarantee the new entity would avoid disbanding or eliminating significant portions of service, he says.

Political views

Current and former politicians have weighed in on the mergers, too. U.S. Rep. Danny Davis (D-Ill.) and Pennsylvania State Rep. Parke Wentling support CN-KCS, while Byron Dorgan — a former U.S. senator and representative from North Dakota — sent a letter to the STB backing CP-KCS. During his Senate career, he repeatedly expressed concerns about how additional consolidation in the rail industry would affect shippers, Dorgan wrote.

“However, the proposed CP-KCS is the one unique transaction among large U.S. railroads that I believe is beneficial and that does not raise the concerns related to East-West transcontinental railroad mergers,” he said.

Meanwhile, U.S. Rep. Peter DeFazio (D-Ore.), who chairs the House Committee on Transportation and Infrastructure, believes both merger bids could signal a wave of rail consolidations that might stifle competition and prompt industry-wide consolidation.

But many rail industry analysts disagree with that assertion since any combo besides CP-KCS would trigger the STB’s more stringent merger rules.

While insiders and observers continue to weigh the proposed mergers’ merits and detriments, CP and CN figure to keep promoting their respective KCS marriages. Creel and Ruest zeroed in on potential benefits during their Q1 earning conferences in April.

Said Creel: “There would be multiple fronts, new routes, new markets and new competition introduced. Customers get reached today with this combination — when approved, and we believe it will be — that quite frankly without it is impossible.”

Said Ruest: “The combination will significantly enhance customer’s choice and competition. In particular, it would create a new express route that connects the U.S., Mexico and Canada with end-to-end seamless single-owner, single-operator service. It would connect CN and KCS buyers and sellers to more destinations, [and] preserve access to all existing interchange options to enhance route choice and ensure robust competition.”

Email questions or comments to jeff.stagl@tradepress.com.

CN-KCS: Another major merger to mull over

Rail industry constituents, analysts and observers were still trying to decipher the implications of the proposed CP-KCS merger announced March 21 when CN unveiled its own competing bid for KCS a month later.

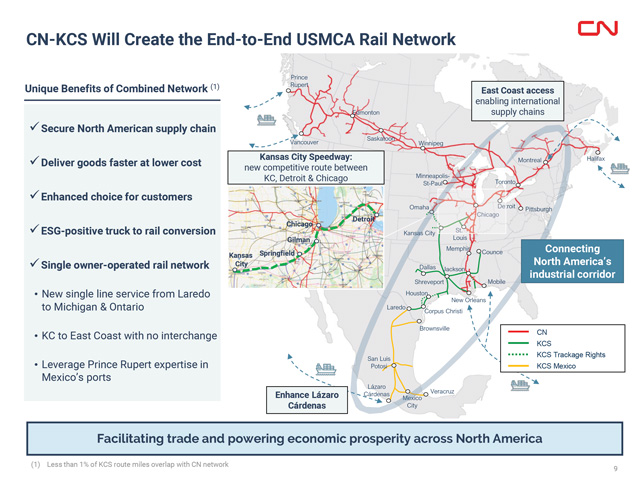

CN proposes to combine with KCS in a cash-and-stock transaction valued at $33.7 billion, or $325 per share. CN-KCS would connect North America’s industrial corridor, and add more fluid and cost-efficient transportation options across such network points as Detroit, Laredo, Texas, and southern Ontario, CN officials said in a press release.

“CN is ideally positioned to combine with KCS to create a company with broader reach and greater scale, and to seamlessly connect more customers to rail hubs and ports in the U.S., Mexico and Canada,” said CN President and Chief Executive Officer JJ Ruest.

CN leaders sent a letter to KCS’ board outlining their proposal, under which KCS would continue operating under its name in the United States and Mexico. CN-KCS would require the formation of a voting trust and Surface Transportation Board (STB) approval; CN submitted an associated pre-filing notification to the STB.

On April 24, KCS announced its board found CN's proposal could be reasonably expected to lead to a “company superior proposal” as defined in the CP-KCS merger agreement. KCS will provide CN with nonpublic information and engage in discussions and negotiations — subject to requirements of the CP agreement — although its board gave no assurance the talks would result in a merger agreement.

The competing bid irritated CP leaders, who believe it’s illusory, inferior, massively complex and likely to fail, and increases regulatory and antitrust risks.

In addition, the promise of $325 per KCS share is unattainable, said CP President and CEO Keith Creel during the Class I’s April 21 earnings conference.

“Unrealized value is still equal to zero. If you can't do the deal, it's not doable,” he said.

Moreover, CN-KCS would be anti-competitive and reduce shipper service options at more than 100 locations — network overlaps that greatly exceed the 65 miles of track in Louisiana cited by CN, Creel said.

“How many customers, multiple customers, are losing service options?” he posited.

However, CN leaders are convinced their merger proposal is solid because it promises strong shareholder benefits, earnings synergies approaching $1 billion, facilitated trade and new revenue opportunities.

CP: CN-KCS likely to fail

CN-KCS offers high financial value over the immediate and long terms, is a more complementary strategic fit, and promises greater choice and efficiencies for customers, said Ruest.

CN’s proposal is financially superior and strategically compelling, but might entail a more complicated regulatory review, given the larger rail network that would be created, said Robert W. Baird & Co. Inc. Senior Research Analyst Garrett Holland in an April 20 report. CN-KCS — which would become the third-largest Class I — probably would elicit more objections, he believes.

“CP likely revises its bid higher and leans into the strategic value of the combination and potentially more feasible regulatory review process,” Holland wrote.

CN’s case and economics seem cogent, said independent rail industry analyst Tony Hatch in an April 20 report. Although the deal is more complex, the market — and not regulators — ultimately will decide who combines with KCS, he wrote.

“Both deals would pass the STB approval process, the CN [one] with more conditions,” Hatch wrote. “The assertion that CN’s [proposal] is less problematic is wrong, however.”

The bidding war between CN and CP ultimately will impact any financial upside due to a very healthy valuation that’ll be paid, wrote Stephens Inc. analyst Justin Long in an April 21 report.

“Simply put, the winner will have a lengthy regulatory process and years before a meaningful amount of financial accretion is realized, and the loser will face the challenges of a larger competitor,” he wrote.

— Jeff Stagl

Keywords

Browse articles on Canadian Pacific CN Kansas City Southern Class I mergers Surface Transportation Board Tony Hatch Allison Landry David Vernon Garrett Holland Justin Long North Dakota Grain Shippers Association Soy Transportation Coalition rail shippersContact Progressive Railroading editorial staff.