Creel: CP-KCS is best combination based on ‘undeniable truths’

4/23/2021

Editor's note: This story was updated April 24.

By Jeff Stagl, Managing Editor

On April 21, Canadian Pacific President and Chief Executive Officer Keith Creel began the Class I’s first-quarter earnings conference thusly: “Certainly, we've got some exciting things to talk about.”

He wasn’t referring to CP’s Q1 financial performance. Instead, Creel wanted to “address the M&A buzz that’s in the air,” meaning CP’s merger agreement with Kansas City Southern and CN’s rival bid. And he proceeded to talk about those competing proposals for a half-hour.

CP plans to acquire KCS stock in a cash transaction announced last month worth $29 billion, including $3.8 billion of outstanding KCS debt, while CN just recently unveiled a proposal to combine with KCS in a cash-and-stock transaction valued at $33.7 billion, or $325 per share.

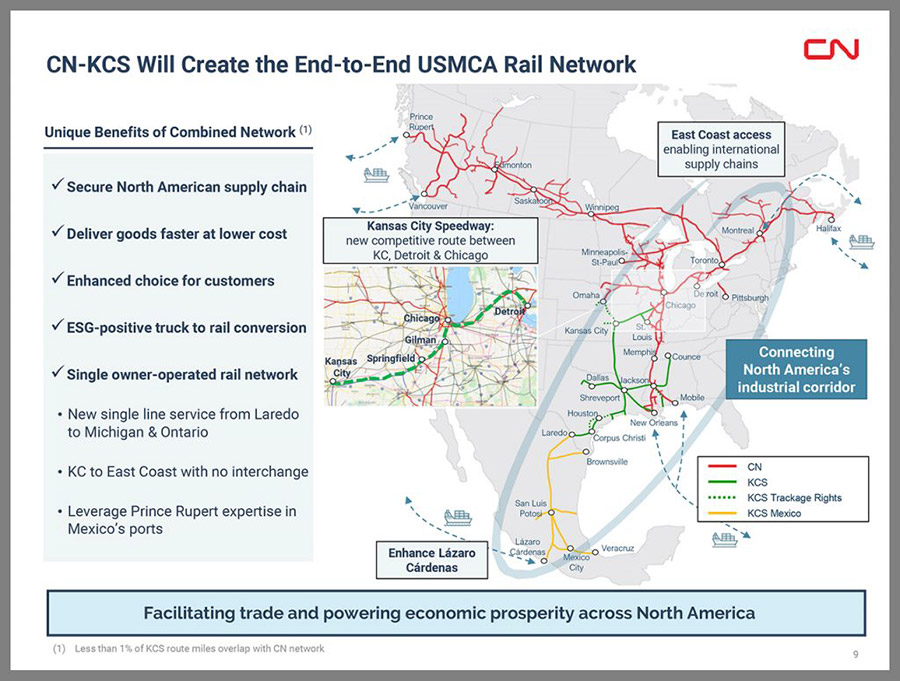

CN leaders are convinced their merger proposal is superior because the end result would be a premier Canada-U.S.-Mexico rail network, strong shareholder benefits, earnings synergies approaching $1 billion, facilitated trade, new revenue opportunities, a broader reach and greater scale, and more seamless connections to rail hubs and ports.

CP leaders claim the combination with KCS would enhance competition by creating new and stronger competitive single-line options, take more trucks off highways, preserve the basic six-railroad structure of the North American rail network, expand customers’ network reach and provide new competitive transportation service options.

“Rather than acknowledge the clear and substantial superiority of CN’s proposal for KCS shareholders, CP has sought to distract investors and attack CN’s proposal with a variety of inaccurate and unfounded assertions,” CN President and CEO JJ Ruest wrote in an April 22 letter to KCS' board. Credit: CN

“Rather than acknowledge the clear and substantial superiority of CN’s proposal for KCS shareholders, CP has sought to distract investors and attack CN’s proposal with a variety of inaccurate and unfounded assertions,” CN President and CEO JJ Ruest wrote in an April 22 letter to KCS' board. Credit: CNThe CP-KCS combination wins out when each proposal’s claimed benefits are placed under the microscope of “undeniable truths,” Creel said.

“I think the best and only way to address those points and, frankly, anything tied to what is truly the only unique and unparalleled strategic value opportunity combination, is with the truth [and with] undeniable facts,” he said.

CP-KCS would be the only true United States-Mexico-Canada Agreement network and opportunity, and the only Class I combination that could pass the Surface Transportation Board’s public interest test, Creel believes.

“It would be the only one, not one of many, the only. Why do we say that? Why is that true? Why is that undeniable? It's pro competitive,” he said. “There would be multiple fronts, new routes, new markets and new competition introduced. Customers get reached today with this combination — when approved, and we believe it will be — that quite frankly without it is impossible.”

The combination also promises to unlock attainable value for CP and KCS shareholders.

“This deal is approvable. It's doable. And in order to realize the value, you’ve got to get the deal done,” said Creel. “There's over $800 million of conservative synergies that we've spoken to, that this deal represents for our shareholders to benefit from.”

Source: Canadian Pacific

Source: Canadian PacificOther points stressed by Creel: CP-KCS would be pro-service, creating service where it doesn't exist for many customers; wouldn’t impact existing service or reduce options for any customer; would prompt additional investments to create capacity on the railroads’ lines; and would unlock attainable value for shareholders. The proposed merger also has received a lot of support from customers and business partners — more than 400 of them filed statements with the STB favoring CP-KCS.

All of those reasons and more lead to one undeniable truth: deal certainty, Creel said.

“This deal represents the path to true realized value, compelling value now and the value it represents and even more compelling … the long-term sustainable value that is only uniquely created by this combination. Those are undeniable truths,” he said.

Conversely, the CN-KCS deal offers a “headline value number” of $325 per KCS share that’s undeniably eye opening, but in reality is unattainable, Creel believes.

“Unrealized value is still equal to zero. If you can't do the deal, if it's not doable, you'd never get there,” he added.

Creel also stressed that CN-KCS would be anti-competitive and anti-service, reducing shipper service options at more than 100 locations — network overlaps that greatly exceed the 65 miles of track in Louisiana cited by CN.

“Come on, man that's not the truth. How many customers, multiple customers are losing service options?” Creel posited. “How many customers today that just CP and CN alone enjoy an opportunity to choose between the two of us, in partnership with KCS lose that option?”

There already has been an overwhelming outcry of opposition to CN-KCS from customers, according to Creel.

Source: CN

Source: CN“The truth is if you're in the ag industry and you happen to be located in North Dakota, South Dakota, Minnesota, Iowa, in the Green Belt of America or in Middle America, this deal represents a lost opportunity. This deal strands your product. This deal says you never enjoy single-line service that the CP-KCS provides or creates,” he said.

Creel then cited what he characterized as the biggest undeniable truth about CN-KCS: deal uncertainty.

“The headline value could be 500% more than our real attainable value. It's fantasy money. It's fool's gold,” he said. “I know the team at the KCS. I've got a deep respect for them. They understand what pro-competition means and what pro-service means.”

At the end of the day, investors will make the final decision.

“I think if you're an investor and you look at what story you believe, what represents truth? I think the train that you want to join, the train you want to get aboard is the one that's most probable based on not what they say, but what they've done,” Creel said. “Our story at CP, it's a story of doing what we said we're going to do. It's a story of turning this company around, taking this proud talented group of railroaders and creating a unique value in this industry.”

In a letter sent April 22 to KCS’ board — clearly after CP’s earnings conference — CN President and CEO JJ Ruest addressed Creel’s comments.

“Rather than acknowledge the clear and substantial superiority of CN’s proposal for KCS shareholders, CP has sought to distract investors and attack CN’s proposal with a variety of inaccurate and unfounded assertions,” Ruest wrote. “CP’s claims are not intended to benefit KCS shareholders, but to advance CP’s own interests and to deprive KCS shareholders of the full value for their shares.”

The regulatory approval condition that’s relevant to KCS shareholders is approval of a voting trust, and CN is proposing to use the identical voting trust that CP has proposed, he said. CN is confident the Surface Transportation Board will not subject CN’s proposal to any different standard or scrutiny in approving its voting trust than would be applicable to CP’s proposal.

“CP’s deliberately misleading claims to the contrary are not correct. CN’s proposed combination is clearly in the public interest, and will enhance competition and produce substantial benefits for customers, communities and employees,” Ruest wrote. “Following the closing of the voting trust, CN is confident that it will be able to effectively address any reasonable remediation concerns and ensure that rail customers and other stakeholders benefit from the proposed combination with KCS.”

On April 24, KCS announced its board had "unanimously determined, after consultation with the company's outside legal and financial advisors," that CN's "unsolicited proposal ... could reasonably be expected to lead to a 'Company Superior Proposal' as defined in the CP-KCS merger agreement."

As a result, KCS will provide CN with “nonpublic information and to engage in discussions and negotiations with CN with respect to CN’s proposal,” subject in each case to the requirements of the CP merger agreement, KCS said, adding “there can be no assurance that the discussions with CN will result in a transaction.”